Answer this question: "How much profit should we make?" I'll bet your answer was one of the following: "5percent, 10 percent or 15 percent. More! As much as I can get!" In a recent survey I conducted of more than 2,500 construction company owners, I learned:

• 66 percent of companies have no specific profit goals

• 70 percent of companies have no overhead goals

• 50 percent of companies have no sales volume goals

• 92 percent of all company employees have no written goals.

Shoot for Nothing, Hit it Every Time

Most companies shoot for moving targets by attempting to make "as much money as possible" or"more" than they are currently making. "As much money as possible" is not a target. "More!" More than what? These are not clear targets or goals. Five percent, 10 percent or 15 percent are not clear targets, either. As your sales and job costs vary each month, your total markup earned changes, while your fixed cost of doing business remains the same. This causes your net profit to move up and down like a roller coaster.

After hearing me speak at a convention, a young contractor asked me for advice. He told me his five-year goal was—not in these exact words—to work too hard, make every decision himself, putout fires, keep his crews busy, be totally stressed out, not make enough money to hire the best people, get hopelessly in debt and make no money. And, the bad news was, he had achieved his goal! I am not impressed with people who are busy,overworked, underpaid or boast about their latest sales conquests. I admire organized companies that hit their specific bottom-line profit goals and make the expected return for the risk they take.

A specific annual sales target of $3,000,000, an overhead target of $400,000 and a net profit goal of$120,000 are specific fixed targets you can shoot for and hit. Not "more." Not "as much as possible." Consider these questions:

- What is your annual sales target?

- What is your annual overhead budget?

- What is your annual net profit goal?

Always Make a Profit

The goal in business is not to stay in business or keep your crews busy. The goal of doing business is to always make a profit. According to a recent Construction Financial Management Association study, companies that have specific strategic plans with clear targets and goals make 33 percent more profit than companies without targets. According to Concrete Construction magazine, only 33 percent of all contractors actually make a profit every year. Additionally, 92 percent of all business owners reach age 65 with $0 net worth! It's not how much you make that matters,it's how much you keep (after overhead, job costs, staff and a fair salary for the owner).

Run Your Company Like a Business

When I present my program "How to Build a Construction Company That Always Makes a Profit" at conventions, I repeatedly learn that most small- and medium-sized general contractors and subcontractors do not run their companies like a business. A "business" has a business plan, sales goals, job cost goals, an overhead budget and profit goals. A "business" pays its president or owner a fixed and reasonable salary every month (plus year-end bonuses from the net profit). A "business" prepares monthly financial statements,profit-and-loss statements, income statements and balance sheets. Most importantly, a "business" makes a profit.

A "business" without all of the above is not a "business." It is a place to go to work, a place to try to make some money, a place to try to cover expenses and a place to try to have some leftovers to pay for the owner's lifestyle.

Get a Return on Your Investment

If asked to invest $100,000 in a friend's new start-up contracting business, what annual return would you want? Ten percent, 15 percent, 25 percent, 50 percent or more? After considering the risks, I would never invest in a new construction business that didn't offer at least a minimum guarantee of 15 to 20 percent annual return on investment. Your fixed cost of doing business (overhead) is an investment in your future ability to make a profit, as well. Every year you decide what overhead costs you will need to run your business. You staff accordingly, rent an office, seek jobs to bid and hope enough business comes into make a profit. Likewise, you must also make a minimum 15 to 20 percent annual return on the fixed overhead investment you commit to in advance every year.

Aim at a Fixed Target

Contracting companies should make a minimum 20 percent return on overhead every year. This is the minimum target to shoot for. If your annual overhead is $400,000, you should expect a minimum net profit pretax of $80,000. Remember, this is the minimum. The minimum to me is way too low to shoot for. I recommend aiming at a target of 40 percent to 50 percent return on overhead. For example, if your overhead is $400,000, your pretax net profit goal would be $160,000 to $200,000. Now you have a minimum target and a higher target to shoot for. These are specific goals you can aim at, tracking your progress as you go.

What is Your Fixed Cost of Doing Business?

First, determine your fixed cost of doing business, or annual overhead costs. Overhead costs include everything you need to run your business without any jobs in progress. Overhead costs include:

- company management

- administration and accounting

- estimating

- marketing and sales

- your office and utilities

- computers and supplies

- all non-job business costs.

Job costs are not a part of your overhead. They include everything that occurs out in the field or on the job site and must be job-charged. Your job costs should include:

- project management

- supervision

- pro-rata share of owner for project management or supervision time

- all field labor

- field labor burden and fringe benefits

- field workers compensation insurance

- liability insurance for jobs and labor

- field trucks and equipment.

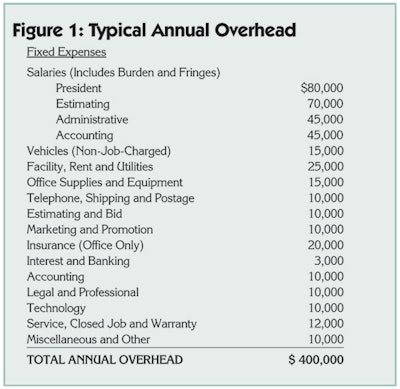

A typical $3,000,000 contracting company's overhead is shown in "Figure 1: Typical Annual Overhead." Your task is to calculate your accurate fixed annual cost of doing business. This is the 'nut' you have to crack before you can break even every year. Always include a fair and reasonable salary for the owner or president of your company. If your owner runs some jobs,split his or her time between overhead and job costs such as project management or supervision. Also, field labor job costs must include workers compensation insurance and liability insurance. These are not overhead charges,as they don't occur unless your field crews are working on jobs. Be sure to put those costs into your job charge and not into overhead. Another mistake I see is putting all of your company vehicles into your overhead. Most vehicles are used out in the field and should be job-charged including the insurance, gas and maintenance.

Markup vs. Gross Profit

To make a profit after paying all of your overhead and job costs, you must know the markup and gross profit you can make in the market in which you compete. For starters, be aware of the difference between markup and gross profit. Markup is the percentage you mark up your job costs when bidding a job. Gross profit is the total overhead and profit you make as a percentage of total sales. See the examples and formulas in the "Markup vs. Gross Profit" sidebar for converting markup to gross profit.

Track Your Bottom-Line Performance

One of the best ways to determine the markup and gross profit you can expect in your competitive market is to look at your trends on completed jobs. That's why you should keep a completed jobs chart handy and updated at all times. Include the start date, job name, project manager,superintendent, foreman, contract amount, bid markup, final actual markup you made and the gross profit percentage you actually made after project completion. (See "Figure 2: Completed Contracts") Study the competition and economy trends to determine what sort of markup you can hope for on future jobs based on what you have been getting.

Volume and Sales Goals

You are now ready to determine what sales target you must hit to achieve your net profit goal. You know your fixed cost of doing business or annual projected overhead. You have a pretax net profit goal of 20 to 40 percent return on overhead. You are tracking the trends of your completed jobs and are aware of the markup and gross profit you can get in the marketplace in which you compete. Now it's time to figure out how much volume you need to hit your goals.

Looking at the seven-step formula to always make a profit shown in Figure 3, the company's annual overhead is projected at $400,000. The return on overhead goals is 20 percent minimum with a high target of 40 percent. This gives the company a minimum pretax net profit goal of $80,000 and a high goal of $160,000. This will require a total gross profit to achieve the overhead and profit targets of $480,000 and$560,000 accordingly. By studying completed contracts and looking at the market trends, the company determines it can achieve a 20 percent total overhead and profit markup and a16.67 percent gross profit margin. To determine how much volume they need to hit their goals, divide the total gross overhead and profit projected(#4) by the gross profit percentage anticipated (#6). ($480,000 / .1667 =$2,879,424 annual sales at an average markup of 20 percent)

This is the best way to determine the total sales you need to hit your goals. Companies without precise overhead and profit goals never make enough money and probably won't make a profit. It's hard to hit a target that doesn't exist. Companies that track costs, target profit, control overhead, watch what they keep, are organized and remain in control stay one step ahead of their competition. Fix your overhead, set clear profit targets and then shoot for the revenue you need at the markup you can get to achieve your goals. Keep targets in front of you all the time. Share them with your people. Track your progress. Make it happen. See you at the bank!