Buying a home is a better financial decision than renting for most buyers who intend to live in a home for at least three years, according to real estate research firm Zillow.

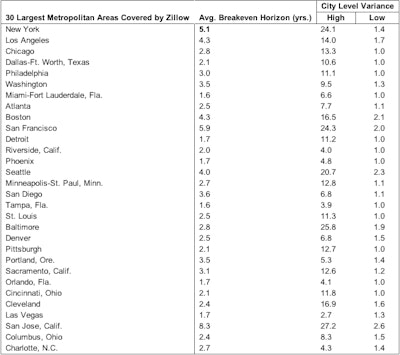

In some metro areas where home values fell dramatically during the housing recession, Zillow determined, homebuyers break even after less than two years of owning a home. Further, Zillow determined that the Miami/Ft. Lauderdale metro area is among the most favorable for buying, with homeowners breaking even after only 1.6 years of living in the home. However, in the San Jose metro, where home values are among the highest in the nation, a buyer must commit to living in their home for 8.3 years before they will break even.

"Across most of the country, historic levels of affordability make buying a home a better decision than ever, especially considering rents have risen more than 5 percent over the past year," said Stan Humphries, Zillow's chief economist. "This is the first analysis of metros and cities that presents the buy versus rent decision in an intuitive way, by telling consumers how long they must live in the home before buying breaks even with renting financially. It's much more understandable, and therefore useful, than the abstract notion of a simple ratio of prices to rents. If we want consumers to act on market information, we have to align it with how they think about the issue and make it straightforward to grasp."

In its study, Zillow analyzed the "breakeven horizon" in more than 200 metros and 7,500 U.S. cities to determine how many years it would take before owning a home becomes more financially advantageous than renting the same home. In more than 75 percent of metro areas analyzed, a homeowner would break even after three years or less of owning a home.

All possible costs associated with buying and renting were incorporated into the analysis, including down payment, mortgage and rental payments, transaction costs, property taxes, utilities, maintenance costs, tax deductions and opportunity costs, while adjusting for inflation and forecasted home value and rental price appreciation.