Although many wood flooring pros feel positive about 2019, others are cautiously watching the predictions for housing this year and tempering their expectations. What else did we find out in our exclusive State of the Industry survey (which we have published since 1992)? To discover more helpful data from wood flooring manufacturers, distributors, retailers and contractors, keep reading.

Manufacturers

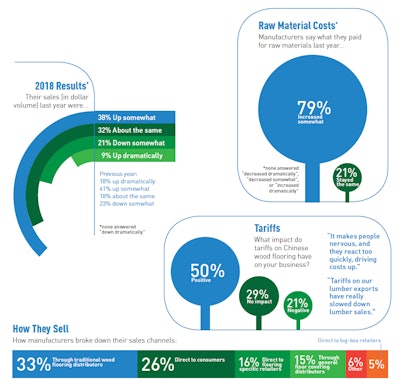

Here are the results from the wood flooring manufacturers who participated in our online survey in January.

Armstrong's hardwood flooring segment: a timeline

After two decades as the largest and one of the most influential wood flooring manufacturers in the industry, Lancaster, Pa.-based Armstrong Flooring completed the sale of its entire wood flooring segment to a private equity firm on Dec. 31, 2018, for $100 million.

The sale of its hardwood flooring business, which produced Armstrong Flooring, Bruce, Capella, HomerWood, T. Morton and Robbins wood flooring brands, came after three years of declines in hardwood flooring sales.

"The wood flooring industry has been impacted by changing market dynamics," Armstrong Flooring CEO Don Maier stated in the announcement of the sale, "and now is the right time to deepen our focus on LVT and other resilient flooring categories, where we are confident fundamentals remain strong for future growth."

The conglomerate of brands and six U.S. manufacturing facilities began a new era in January 2019 as AHF Products, a Lancaster, Pa.-based company formed by private equity firm American Industrial Products (AIP).

The following timeline traces Armstrong's rise to the top in the wood flooring industry and its eventual exit.

1978 – Triangle Pacific Corp. (Dallas), a cabinetry maker, buys Bruce Hardwood Floors (Dallas). Bruce would spend the '80s becoming the largest producer of residential hardwood flooring in North America.

1996 – Triangle Pacific buys Hartco Flooring Company (Knoxville, Tenn.), one of Bruce's biggest competitors, from Premark International for $63 million, according to Neil Moss, a former regional manager with Hartco and later with Armstrong. Premark had purchased Hartco in 1988 for $94 million and invested about $30 million building a new manufacturing facility prior to the sale to Triangle Pacific.

1997 – Completing a quick one-two punch, Triangle Pacific also buys the residential flooring operations of Robbins Inc. (Cincinnati) and Robbins-owned Searcy Flooring. The acquisition brings Triangle Pacific's U.S. market share to 46 percent, the company reported, with $653 million in revenue that year.

1998 – Armstrong World Industries (Lancaster, Pa.), a Fortune 100 company and a massive producer of sheet vinyl, buys Triangle Pacific for approximately $890 million and assumes about $260 million of the company's debt. Two weeks prior to the purchase, Armstrong had bought DLW, a major European hard-surface flooring manufacturer. After the acquisitions, the company's annual flooring revenue is estimated to be in excess of $2 billion.

2000 – Armstrong declares bankruptcy after litigation regarding its manufacture of asbestos during the 1960s. Triangle Pacific announces that it and its subsidiaries (Bruce, Hartco and Robbins) will not be impacted by the parent company's bankruptcy filing.

2006 – Armstrong purchases Capella Engineered Wood LLC (Vicksburg, Miss.) and HomerWood Hardwood Floors (Titusville, Pa.), with annual sales of $15 million and $26 million, respectively. Later in 2006, Armstrong's plan of reorganization is approved, and it emerges from bankruptcy six years after filing.

2007 – Armstrong expands Patriot Hardwood Floors and Supply Inc. (Wilmington, Mass.), a distributorship included in Armstrong's purchase of Triangle Pacific in 1998, into Connecticut, New York and parts of New Jersey. Patriot continues to service its existing territory in Maine, Massachusetts, New Hampshire, Rhode Island and Vermont. That same year, Armstrong launches its own distribution company, Armstrong NW LLC (Seattle), to distribute its products to specialty retail stores and flooring contractors in Washington, Oregon, Montana, Wyoming, Idaho and Alaska.

2009 – Armstrong lays off about 200 workers with plans to eliminate 425 positions in 2009, affecting plants in Jackson, Tenn.; West Plains, Mo.; Center, Texas; and Vicksburg, Miss. "The sales volume isn't there, and to stay viable as a business we must control cost," a spokesperson for the company says.

2010 – Armstrong lays off 260 workers at its hardwood flooring plant in Oneida, Tenn., and 60 at its plant in Center, Texas, citing a lack of demand in the residential market. The Oneida location (formerly a Hartco plant) shuts down its strip mill, finish line and yard operations.

2011 – The lack of demand continues, and the company announces more layoffs, this time of 116 employees at its wood flooring plant in Beverly, W.Va.

2012 – Armstrong sells Pompton Plains, N.J.-based distributor Patriot Flooring Supply Inc. (formerly Patriot Hardwood Floors and Supply Inc.) to Mansfield, Mass.-based distributor Belknap White Group. "Patriot distributes hardwood and laminate flooring, and we're in the business of making and marketing floors," Armstrong's flooring CEO Frank Ready says of the sale at the time.

2014 – Armstrong says it will exit DLW, its European flooring business purchased in 1998. Since 2007 Armstrong had invested $150 million in the company, which did not generate a profit. It also closes its engineered hardwood flooring facility in Kunshan, China, and relocates its operation to Somerset, Ky.

2015 – The company announces it will split its flooring business from its ceilings business and create two independent and publicly traded companies, with the ceiling business remaining Armstrong World Industries and the flooring segment operating under the name Armstrong Flooring.

2018 – Armstrong gives distributors increased responsibility for the marketing, merchandising and sales of its residential flooring products and cuts back on its in-house marketing. The reorganization leads to about 100 layoffs. Following declines in its wood floor sales, the company announces in November it will sell its wood flooring segment to AIP for $100 million in order to focus on its resilient flooring operations.

2019 – AIP establishes AHF Products, an independent wood flooring company that will take over the former Armstrong wood flooring segment and maintain its brands. Brian Carson, a former senior VP of operations for Armstrong World Industries and the former president of Mohawk Industries (Calhoun, Ga.), is named president and CEO. Carson announces he aims to launch a record number of new products and initiatives in the inaugural year of the standalone company.—R.K.

Distributors

The distributors responding to our survey were 77 percent wood flooring specialists and 23 percent general floor covering distributors.

A shifting wood flooring market after Chinese flooring tariffs

It has been a hectic past seven months for many companies that have relied on importing or exporting Chinese wood flooring for their business. The Trump administration's levy of an additional 10 percent tariff to all types of wood flooring from China in September 2018, with an ongoing threat of increasing it to 25 percent (still unsettled as of press time of this issue), spawned in-kind retaliation from the Chinese government and rattled segments of the wood flooring industry here in the United States. The trade war's impact, suppliers say, could alter the way the industry ticks.

But as big of an impact as the new trade war has had in the industry, the increased instability of the trade between the two countries wasn't entirely unexpected by wood flooring suppliers and distributors with skin in the game.

The first signs of disruption "We started to move out of China several years ago, largely because of the antidumping duty on multilayer wood flooring," says Danny Harrington, VP of marketing and product development at Santa Fe Springs, Calif.-based Galleher LLC. "The way the U.S. trade policy is applied retroactively makes for a very unpredictable cost structure."

The U.S. imposed preliminary antidumping countervailing duties on certain engineered wood flooring from China in 2011 after an investigation determined multiple Chinese manufacturers had been producing and selling engineered wood flooring at an unfairly low price.

"All of the headache that we went through on the anti-dumping countervailing duty matter really set us up to be ready to handle this issue," says Sam Cobb, CEO of West Plains, Mo.-based Real Wood Floors. "The industry was already looking for somewhere else to go." In Cobb's view, the tariff on its own didn't amount to much more than a typical annual price increase, but when combined with the anti-dumping duty already in place, it became potent.

The U.S. reaction It was a need-to-hit-the-ground-running kind of moment for companies when the new tariffs were unveiled after two weeks of public hearings at the Office of the U.S. Trade Representative.

"It kind of came as a surprise to everyone that they moved as quickly as they did when they said to go ahead and levy the 10 percent," says Cobb, who testified against the tariffs during the public hearings. Numerous companies eventually announced price increases, many with the hope it would be a temporary measure.

The 25 percent tariff possibility, which President Trump delayed several times since its announcement, has caused flux and uncertainty in the industry.

"It's been a very, very busy fall and winter for me," says Harrington, noting he's flown to Asia twice this year already and to three Eastern European countries as he explores new facilities.

To get ahead of another possible price increase, Real Wood Floors purchased more flooring in the past quarter than ever before. Cobb has also moved almost all of his company's production out of China in the relatively short period. "There's just not really an option to stay there," he says. "It's not good business. Too many unknowns."

The China reaction The Chinese wood flooring industry's reaction to the tariffs has been largely what some in the U.S. industry had anticipated: They moved quickly.

Recently, Chinese wood flooring companies have opened two factories in the U.S., two in Ukraine and six in Cambodia, according to Cobb. In December, Cobb visited seven wood flooring mills in Vietnam—six of them were Chinese-owned.

Should Chinese companies manufacture in Vietnam or Cambodia, the two countries where much of the wood flooring production in China appears to be moving, Cobb says wood flooring will likely be even cheaper than it was in China due to lower tariffs and labor costs–precisely the opposite intended effect of the tariffs.

"This goes back to anti-dumping," says Cobb. "It's not a China issue. Because if you take China out of the picture, it's going to pop back up in some other country … it's already happening that way."

The long-term impact In recent months, the U.S. and China have been in negotiations to end the trade war and have reportedly been taking positives steps to that end, with President Trump delaying the threatened 25 percent tariff increase indefinitely and discussing rolling back the 10 percent tariff.

In the long haul, Harrington hopes trade with China will stabilize, noting that Chinese manufacturers have been considerably faster at keeping up with industry trends than U.S. manufacturers have been. If the trade war doesn't resolve, he foresees Chinese manufacturers landing on their feet.

"The Chinese consumer is embracing wood flooring now more than any time in the past," Harrington says.

As for U.S. importers relying on Chinese wood flooring without a contingency plan, should the tariffs jump to the threatened 25 percent, "overnight they would become uncompetitive," Harrington says. But he understands why some U.S. suppliers importing from China have been largely inactive while waiting for the trade war to blow over. "This particular industry makes it very difficult to move around," he says.

But move around it did—and quickly, according to Cobb.

"I'm amazed at how fast it moves," Cobb says of the global economy. "And it moves much faster than bureaucracy."—R.K.

Retailers

Of the retailers responding to our survey, 33 percent specialized in wood flooring and 67 percent were general floor covering retailers.

Contractors

Hundreds of contractors responded for our survey. 92% Specialized in wood flooring, while 8% work with all floor coverings.

See the following previous State of the Industry reports:

All Things Wood Floor, created by Wood Floor Business magazine, talks to interesting wood flooring pros to share knowledge, stories and tips on everything to do with wood flooring, from installation, sanding and finishing to business management.